The Donald seems to think he has all the time in the world to end the conflagration he and Bibi started in the Persian Gulf. Today he even told the mullahs to take a hike when they suspended any further negotiations owing to Bibi’s brutal strikes on civilian targets in southern Lebanon and continued violations of the so-called April 13th truce in the Persian Gulf.

Thus, regarding the meandering negotiations of the last 45 days, the Donald averred,

“I don’t care if they’re over, honestly… I really don’t care. I couldn’t care less,”

Brave words, these. And completely, totally and hideously out to lunch, too.

What’s actually just around the corner is an explosion of oil and related energy prices that will make the 1970s look like a Sunday school picnic, but here we have the Donald talking just plain barking idiocy about what comes next:

He also said he wasn’t worried about oil prices, which spiked following the report in Iranian state media that Tehran is vowing to “completely block” the Strait of Hormuz in addition to halting negotiations.

“I think the oil will be dropping like a rock in the very near, you know, the very near distance,” Trump said.

The president of the United States – the alleged sagacious businessman we have purportedly been waiting for – couldn’t be more sadly mistaken about something as basic and straight forward as the price of crude oil, its refined products and related energy commodities: To wit, the Donald is absolutely clueless about the cardinal fact that there is one world oil market and ONE PRICE the planet over.

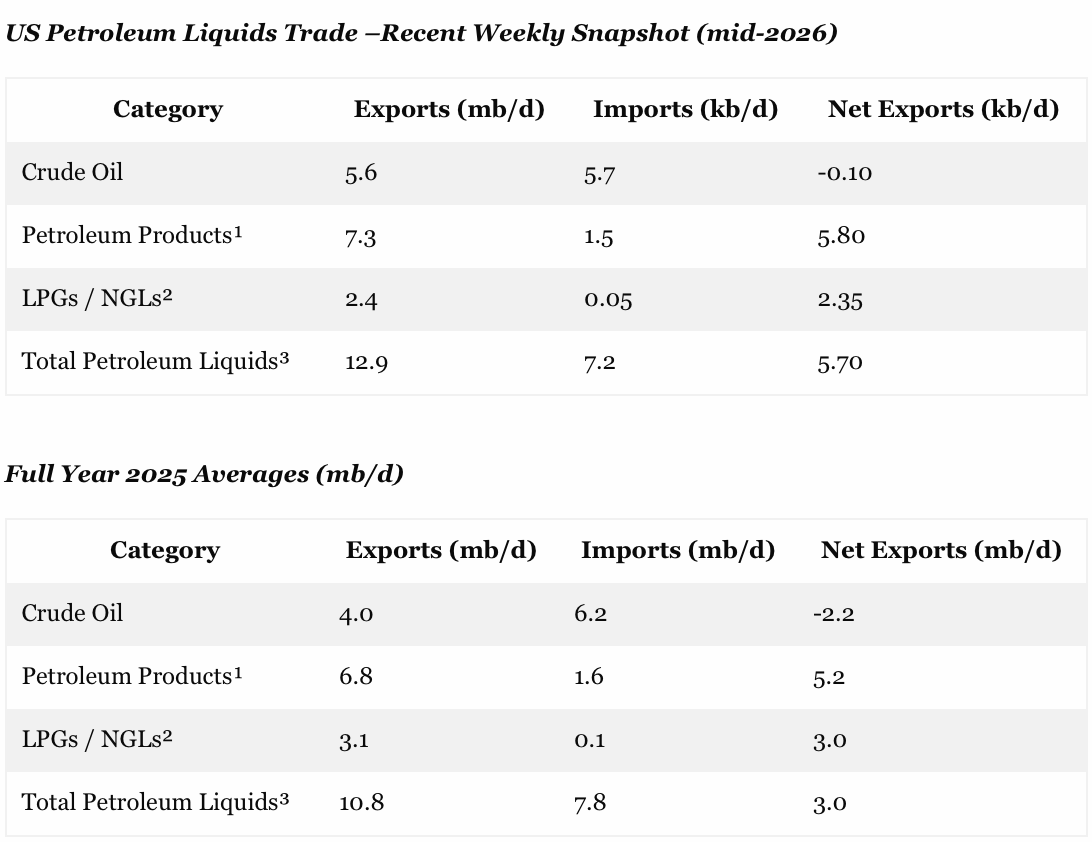

And that’s regardless of the fact that the US is now a large scale net exporter of crude oil, refined products and nat gas liquids. In recent weeks, in fact, the Persian Gulf outages have caused exports to soar 12.9 mb/d, which is up nearly 20% from the 10.8 mb/d average during 2025. In all, current net exports of petroleum liquids at 5.7 mb/d leave not doubt that the USA is solidly “energy independent”.

{kind=link}

But when it comes to the massive Persian Gulf supply outage of upwards of 13 million barrels per day – even after leakage thru both the Iranian and US Navy blockades – so what!

No matter the origin, the destination, the mode of transportation, the precise grade of the crude oil or the mix of refinery output from asphalt to diesel fuel, jet fuel, naphtha and gasoline, it all comes out in the same global supply/demand wash. To wit, traders, producers, consumers, middle men and speculators the world over everywhere and always are on the look out to buy something lower and sell it higher – even after dickering over price adjustments for grade, quality, transportation costs and other incidentals of commerce.

To be sure, there are some leads and lags in the process, but in today’s information rich and instantaneous world, it does not take long for a few missing barrels of supply from the massive petroleum basins upstream of the SOH to work their way through worldwide tradings systems and supply chains and show up at the diesel fuel pumps at corn planting time in Podunk, Iowa.

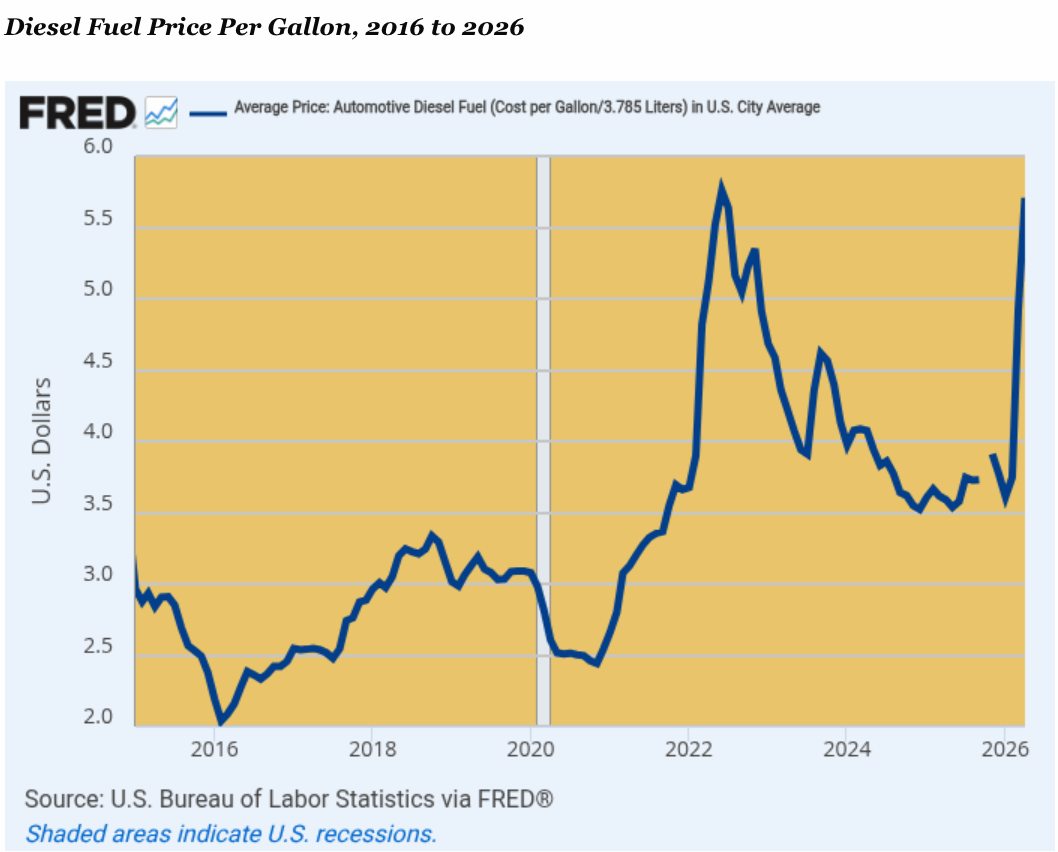

In fact, not withstanding so-called USA energy “dominance” the booming level of total liquids exports shown above, diesel fuel prices on the US domestic market are up by an average of +46% since December 2024, from $3.52 per gallon to $5.71 per gallon. And, as shown in the chart, the latter stands barely a plug nickel below the $5.76 per gallon peak price registered under Sleepy Joe in June 2022.

Needless to say, that upcharge of $2.19 per gallon does not fall silently upon the US supply chain silently like the proverbial tree falling in the empty forest. To the contrary, the US consumes about 170 million gallons of diesel fuel per day in various work fleets which criss-cross the warp and woof of the nation’s $30 trillion GDP. This includes:

- 15 million diesel-fueled work trucks, ranging from rancher pick-ups, to medium and heavy-duty class 4-8 freight haulers vehicles, to semi-trailer-trucks.

- About 2.0 million construction vehicles including excavators, bulldozers, loaders, backhoes, cranes etc.

- Around 4 million diesel-fueled farm tractors, self-propelled combines, balers, forage harvesters and similar equipment.

- Around 39,000 diesel-powered railroad locomotives and and 7,000 work boats operating on rivers, lakes and coastal waterways.

At length, of course, the $170 million per day diesel fuel cost increase incurred by these work fleets get passed on in part or while to customers and their customers down the line to the food aisles and furniture departments of Walmart superstores. In turn, some production doesn’t happen, some weaker links in the supply chains have their profit margins squeeze and some of this $1.2 billion per week up-charge for diesel fuel alone is hitting the bank accounts of retail consumers.

Accordingly, it can be well and truly said that the Donald is just plain out-to-lunch when he thinks that because the US is “energy independent” he therefore has all the time in the world to bring his insane war to a close. In fact, rarely has any POTUS been as dead wrong as is the Donald on the matter of Persian Gulf petroleum supplies:

“We don’t need oil, don’t need the Strait, don’t need anything.” (While touting inflated claims of U.S. production surpassing Russia and Saudi Arabia combined).

In this context, we have focused the case on middle distillates like #2 diesel fuel because it powerfully illustrates the principle of one market and one price in the global petroleum world. In this case, the twist is the broad range of refineries in the world produce vastly different slates of refined products, depending upon their configuration of process equipment; and also upon their input crude oil, which includes a huge range of global supplies ranging from high to low sulfur and heavy to light gravity or molecular structure.

Accordingly, the percentage of asphalt, middle distillates, jet fuel, gasoline, naptha and petrochemical feed stocks which come out of the refinery depend upon the crude oil grades and qualities going in and the configuration of high capital cost and energy intensive process equipment thru which the crude oil passes on its way to the refined product mix.

Needless to say, the Persian Gulf is huge supplier of a wide range of crudes and is also home to upwards of 9 mb/d of refinery capacity – again, with a wide range of process equipment and normal product slates.

Accordingly, the 14-20 mb/d supply outage has had a complex ripple impact on global crude oil and refined product markets. And one of these impacts has been to generate an especially dire shortages of middle distillates in both the Asian industrial economies, as well as Europe. These huge shortages – far higher proportionately for middle distillates than for crude oil overall – have then ricocheted through global markets, causing a huge increase in demand for US based distillate exports, which, in turn, has caused the US domestic diesel fuel price level shown above to rise in lockstep with the worldwide distillate price surge – “drill baby drill” to the contrary notwithstanding.

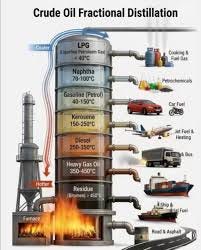

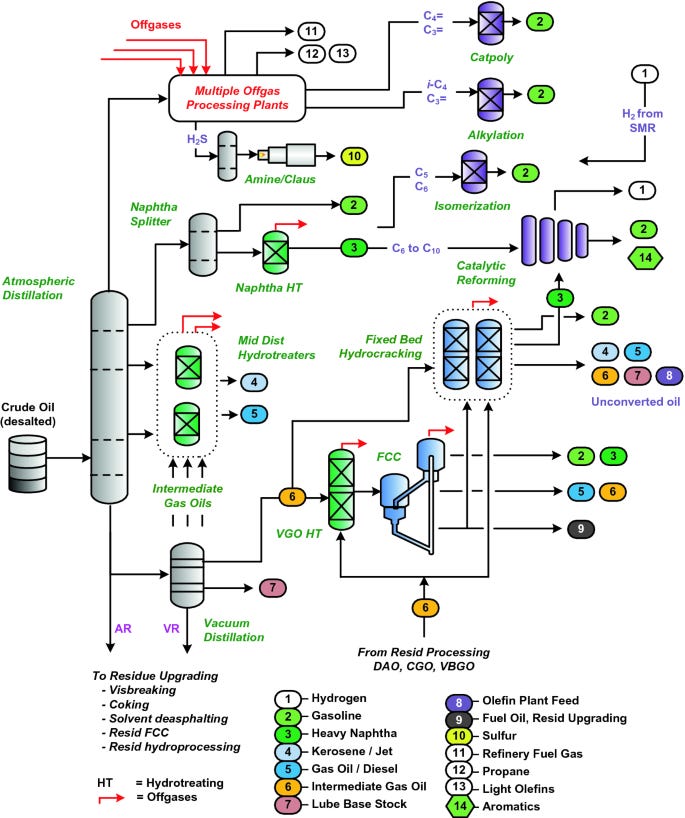

The graphics below provide a simplified version of the product off-take form the front-end or basic refinery distillation tower. This is just the first of a multiplicity of downstream processing units that then shape the mix final refined product, but the point here is that the crude oil input to the distillation tower will generate a wide range of product mixes depending upon its gravity level and other characteristics.

Under today’s refinery technology and economics, however, the product mix yielded from the distillation tower is just the first cut of the crude barrel. Increasing levels of costly downstream processing equipment and stages can alter the initial product yield substantially – again based on both capital investment, cost economics and crude oil characteristics. For instance, yields of gasoline arise from numerous process routes (#2 in green) as does distillate (#5 in blue).

These equipment and process streams, in turn, are optimized to what might be called “steady state” crude oil and product markets and relative pricing among these flows. But when normal crude oil and product flows are drastically and unevenly interrupted around the world, you get a mismatch between the steady state economics of a typical refinery and the altered relative price matrix after the disruption.

In turn, that triggers wide-ranging adjustment in product slates, equipment utilization and the mix of crude oil acquired by refiners and input into the refining run. In the macro sense, Mr. Market goes to work on a worldwide basis.

That is what has happened in the global crude oil and refinery markets in spades. The ordinary bafflingly complex flows of crude oil and products through the global refinery market have now been destabilized seven ways to Sunday. As a result, relative product supply imbalances have reached extreme levels, causing prices and shipment flows to shift in sweeping and unpredictable ways.

Still, what cannot be gainsaid is that all the while the rule of one price is generating constant arbitrage among market geographies and product segments in search of a new equilibrium. The problem, of course, is that a madman and passel of doofuses are calling the shots when it comes to the US War Machine and Washington’s diplomatic posture, meaning that the markets can’t settle down – even as the billiard table of war policy and faux diplomacy in Washington continues to vibrate it radically.

Illustration of the Complexity Of The Global Refinery and Product Markets

In short, the Donald/Bibi attack on Iran on February 28 triggered the most severe disruption to global refined product markets in modern history, particularly for middle distillates – diesel (gasoil) and jet fuel (kerosene). So while the crude oil flows through the Strait of Hormuz (SOH) have dominated headlines, there have been disproportionate impacts on middle distillates stemming from the unique configuration of Persian Gulf refineries and the above described physics of refinery crude yields.

So we next examine the structural differences between the Persian Gulf slates, which are now way short, and U.S. refinery slates – as well as the resulting divergence in distillate versus gasoline crack spreads and volumetric evidence of the disruption’s ripple effects.

Persian Gulf Refineries: Tilted Toward Middle Distillates

The Persian Gulf refineries process predominantly medium-sour crudes (e.g., Arab Light, Arab Medium, Basra grades) with API gravities typically in the 28–34 range and moderate sulfur content. These crudes naturally yield a high proportion of middle distillates include #2 diesel oil upon distillation.

Typical yields for Persian Gulf crudes include roughly 50–60% middle distillates (diesel, jet/kerosene, and gasoil) and only about 20% light ends (gasoline and naphtha), with the balance in heavier residues. Moreover, Gulf refinery equipment configurations amplify this bias. Thus, many facilities, built or upgraded for export-oriented markets in Asia and Europe, emphasize hydrocracking and catalytic cracking optimized for distillate maximization.

In contrast, average U.S. refinery slates lean toward gasoline. U.S. domestic production is dominated by light sweet crudes like WTI (API ~39–42, very low sulfur), which yield approximately 40% light ends (favoring gasoline) and only about 30–40% middle distillates. U.S. refineries, particularly on the Gulf Coast, blend light shale based crude oils with imported medium/heavy sours for optimization, but the overall product slate prioritizes gasoline (often 45–47% of output) over distillates (around 30%).

This mismatch is structural. Persian Gulf refiners are “distillate heavy” by crude chemistry and design, serving export markets hungry for trucking and aviation fuels. U.S. refiners are more “gasoline heavy,” reflecting strong domestic driving demand. When Gulf supply vanished, the world lost barrels disproportionately rich in the products already in tightest supply.

The Post-February 28 SOH Supply Disruption

Following the renewed breakout of kinetic warfare on February 28, 2026, Iranian actions and related hostilities effectively closed or severely restricted the Strait of Hormuz to most commercial traffic. Pre-crisis, the strait carried over 20 million barrels per day (mb/d) of crude and products – about one-fifth of global oil consumption. Post-disruption, loadings plummeted: crude and products through the strait fell from ~20+ mb/d to under 4 mb/d in March and lesser levels in April-May, with alternative routes (Red Sea, pipelines) unable to compensate fully.

In this context, refined product exports from the Gulf were hit hardest. GCC product exports dropped from ~5.0 mb/d in February to 2.1 mb/d in March, with diesel and jet fuel accounting for the bulk of the loss. GCC jet fuel exports to the EU alone fell about 70%, or 370,000 b/d.

Overall Middle East refining runs declined by ~3.1 mb/d in March, part of a global refining cut exceeding 5–6.5 mb/d. This was not merely a crude shock. The displaced crude was medium-sour or precisely the grade yielding the highest middle distillate volumes. Lighter replacement crudes (e.g., WTI, West African) available to other refiners produced more gasoline/naphtha but fewer distillates, exacerbating the imbalance.

Divergence in Crack Spreads: Distillates Surge Relative to Gasoline

The supply shock immediately widened distillate crack spreads (i.e. difference in cost per barrel of crude coming in and the weighted average value per barrel of the product slate coming out of the refinery) far more than gasoline cracks. In global benchmarks like Rotterdam and Singapore, diesel/gasoil and jet fuel premiums to crude skyrocketed in March. U.S. Gulf Coast (USCG) ultra-low sulfur cracks reached peaks around $65–86/bbl, while jet cracks were similarly elevated.

Gasoline cracks, by contrast, also rose (to ~$30–40/bbl range) but lagged significantly. This divergence reflected scarcity: middle distillates faced structural tightness (high export reliance from disrupted Gulf, limited spare capacity elsewhere, and inelastic demand from freight/aviation). Refineries worldwide “flipped the barrel,” maximizing distillate yields by adjusting cuts and conversion units – sometimes by 7–10% of the barrel – sacrificing gasoline output.

The result was a powerful price signal. Distillate cracks strengthened dramatically relative to gasoline, incentivizing complex refiners (especially USGC) to prioritize diesel and jet production for export. This dynamic persisted into April–May, with cracks easing from March peaks but remaining elevated.

Volume Impacts: Reduction from Gulf, Shortages Elsewhere, U.S. Export Surge

On a pre-crisis footing, Persian Gulf product exports (heavily middle distillates) exceeded 3–5 mb/d in key flows. Post-SOH restrictions and refinery outages, GCC refined product exports fell sharply, with diesel and jet comprising the majority of losses.

Europe and the Pacific Rim felt immediate pain. Europe saw GCC diesel/jet arrivals drop 70%, pushing inventories toward critical lows and prompting warnings of systemic jet fuel shortages by summer 2026. Airlines cut flights and raised fares; governments coordinated responses.

In Asia (Singapore hub, India, China), diesel and jet premiums surged, with some countries imposing export curbs or rationing. Pacific Rim buyers competed aggressively for alternative cargoes, diverting barrels from other routes.

The U.S. filled the void. USGC refiners ran at 94–96% utilization, optimizing for distillates. U.S. clean product exports hit records (~3.11 mb/d+ in March, with distillates surging). Distillate exports (diesel + jet) climbed to records of ~1.4–1.9 mb/d in peak weeks/months, up significantly from pre-war February levels.

Jet fuel exports alone more than doubled.As a share of combined U.S. crude and refined product exports, middle distillates rose markedly. Total U.S. energy exports reached all-time highs (~14 mb/d combined in peaks), with distillates commanding a larger portion amid global arbitrage to Rotterdam and Asia. This shift tightened some domestic balances but boosted refining

The Middle Distillate Disruption of 2026: Refinery Slates, Strait of Hormuz Shock, and Global Rebalancing

The sharp rise in global middle distillate crack spreads transmitted rapidly to U.S. refineries, demonstrating that the United States is not an “energy island,” despite the Donald’s constant claims emphasizing complete domestic self-sufficiency. As we have indicated, international product markets operate under the rule of one price, where arbitrage by traders, shippers, and suppliers quickly equalizes values across regions, with only limited time lags driven by freight rates and logistics.

When Rotterdam (ARA) and Singapore diesel and jet fuel cracks surged in March 2026 due to the loss of Persian Gulf supply, the premium created immediate incentives for U.S. Gulf Coast (USGC) refiners to divert barrels toward export. USGC low sulfer (ULSD) diesel cracks, which had been in the $15–25/bbl range pre-disruption, exploded to $60–86/bbl peaks in March before settling but remained highly elevated into May (diesel cracks still averaging well above $50/bbl in recent weeks).

Needless to say, this is not a case of abstract economics. Traders chartered tankers within days, loading ULSD and jet fuel in Houston and Corpus Christi for delivery to Europe and Asia. U.S. refiners, facing the same global benchmarks for products, adjusted operations accordingly: maximizing distillate yields, minimizing gasoline where flexible, and running at 94–96% utilization. The result was higher realized margins at the refinery gate for middle distillates, which in turn fed directly into domestic wholesale and retail prices. The U.S. cannot shield itself from global product pricing signals when it is the world’s largest exporter of refined fuels.

As we showed above, refinery-level distillate cracks and prices have translated into surging diesel fuel prices at the pump for American consumers and businesses. In the most recent weeks of May 2026, the U.S. national average on-highway diesel price hovered between $5.52 and $5.64 per gallon – roughly $1.50–$2.00 above typical pre-crisis 2025 levels and more than 60% higher year-over-year in some measures.

As we indicated, trucking, agriculture, and manufacturing—sectors heavily reliant on diesel – face immediate cost pressures that are now rippling through supply chains. Accordingly, this episode underscores a key reality that the Donald has missed entirely notwithstanding his endless braggadocio about his business acumen: to wit, in integrated global markets for refined products, a supply shock halfway around the world can elevate costs for U.S. drivers and businesses within weeks through arbitrage-driven flows.

Claims of total energy independence overlook this interconnectedness; while the U.S. is a net exporter, domestic prices for middle distillates remain tethered to international benchmarks. And, needless to say, when it comes to the business economics of energy, the Donald well and truly deserves an “F”.

David Stockman was a two-term Congressman from Michigan. He was also the Director of the Office of Management and Budget under President Ronald Reagan. After leaving the White House, Stockman had a 20-year career on Wall Street. He’s the author of three books, The Triumph of Politics: Why the Reagan Revolution Failed, The Great Deformation: The Corruption of Capitalism in America, TRUMPED! A Nation on the Brink of Ruin… And How to Bring It Back, and the recently released Great Money Bubble: Protect Yourself From The Coming Inflation Storm. He also is founder of David Stockman’s Contra Corner and David Stockman’s Bubble Finance Trader.