At the peak of the crisis, oil surged to $110–116/bbl. But it remains volatile at $90–100 after ceasefire pause. Liquefied natural gas (LNG) took an even harder hit. Oil price surged more than 50%, but LNG soared as much as 143% – a 3-year high.

In Asia, supply risk is significant because 20% of global oil and major LNG flows via Hormuz to the region. Here’s the difference between the two sources of the shock. LNG is the binding constraint; oil is volatile but more substitutable.

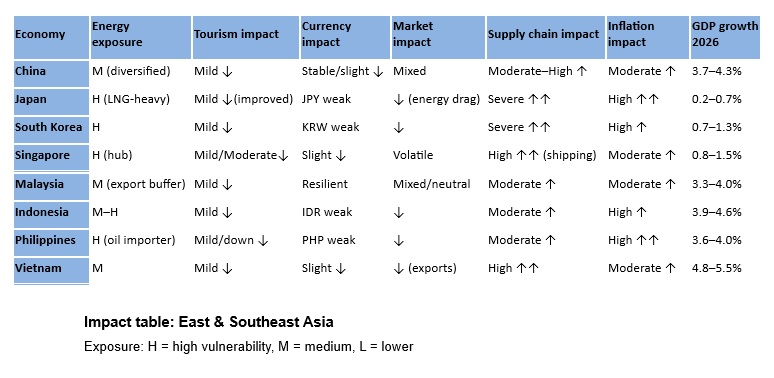

By April 12, the region is overshadowed by LNG tightness, shipping frictions, foreign exchange pressure and already-locked second quarter damage.

What’s compounding the challenges is that Prime Minister Netanyahu’s brutal military campaign in Lebanon severely strained the fragile US-Iran peace talks, which ended without a final deal on Sunday.

This will further downgrade economic prospects in Asia and the world at large.

Inflation, industrial slowdown, bottlenecks…

In energy crises, inflation has always been a dominant transmission channel. A shortage of fuel, electricity and fertilizers means that increased costs for businesses (higher wages, rising shipping costs, higher prices for raw materials) are passed on to consumers across a wide variety of goods and services.

LNG shock tends to result in an industrial slowdown. As prices soar for petrochemicals, plastics, and fertilizers, a major disruption has ensued in Asia, the “world factory.” In this regard, the gas-reliant Japan, Korea and Vietnam are the most exposed.

In shipping and logistics, the Hormuz disruption means higher freight plus insurance expenses, which have resulted in supply chain bottlenecks across Asia.

With foreign exchange and capital flows, oil importers have suffered currency depreciation. As central banks delay rate cuts, tight financial conditions ensue.

Nor is tourism immune to airfare spikes and Middle East airspace disruptions. For now, the impact is moderate. But that could change if the crisis lingers.

Systemic shock

The Iran crisis is primarily an oil/LNG and supply chain shock. In East Asia, it is manifested as industrial squeeze. In Southeast Asia, it is reflected by inflation and the foreign exchange squeeze.

Ceasefire relief does not mean normalization. Due to uncertainty, risk premium persists even if prices dip.

The status quo has deteriorated faster than consensus estimates suggest, as evidenced by the Philippines. Not so long ago, the Marcos Jr. government still suggested that the stage was set for 5-6% growth. Now some multilateral institutions have downgraded the country’s GDP growth to 3.6–4.4%.

Across Asia, growth estimates are being recalibrated. Even the IMF signals broad global downgrade and “permanent scarring.” This crisis is a systemic energy shock.

Why the revisions?

First of all, the LNG shock was underestimated. The foreign exchange and inflation feedback loop has proved more challenging than anticipated. Third, the inventory illusion is fading. Finally, March data still reflected pre-shock inventories but demand compression will ensue in April-May.

Downgrades after downgrades

In Japan and South Korea, the status quo is worse than earlier assumed, due to vulnerability to LNG, petrochemicals and exports.

In Japan, inflation and weak yen have adverse implications. The central bank is reassessing the rate trajectory. South Korea’s GDP growth is likely closer to 1% or below, not 1.5–2%.

As a trade, shipping and refining hub, Singapore remains highly sensitive to freight costs and energy flows. It is facing a large downgrade in percentage terms.

Ever since the first Trump administration, China has been buffered by multiple U.S.-led penalties. But it benefits from Russian energy and diverse policy tools. Though resilient, Beijing must cope with weakening export and industrial demand.

Vietnam is trying to manage its rising supply chain exposure, particularly manufacturing input costs (plastics, chemicals). With lagged effect, the damage is accelerating.

With its very high oil dependence and scarce reserves, Philippines is already facing energy emergency, a currency shock and transport disruptions – amid the greatest corruption debacle and political polarization in decades.

{kind=link}

Risk trajectory if war persists

So, what if the ceasefire fails and the war persists another month?

Oil prices would rebound toward $105–120 as risk premium returns. If the crisis intensifies, they would surge to the $150 territory.

LNG prices would stay elevated and spike further with tight supply. Inflation would surge with a lag in the second and third quarters.

Foreign exchange would suffer further depreciation, especially in Korea (KRW), Philippines (PHP) and Indonesia (IDR). At the same time, supply chains would crumble further with inventories depleted.

Key escalation triggers feature a renewed Hormuz disruption, Qatar LNG outages and crisis expansion to Bab el-Mandeb which would serve as a trade shock multiplier.

According to the IMF, the Iran shock is already affecting 80% of countries. In developing Asia, the crisis could shave off -1.3 percentage points of the GDP growth.

Persistent supply shock

For now, the energy shock remains the largest on record. Downside risks dominate. Growth distributions continue to shift lower. And there are no meaningful upgrades.

As the regional stabilizer, China’s growth hovers around 4.0%, but it is being challenged by weakening exports and softer global demand. Korea and Japan are deteriorating further.

In Southeast Asia, Singapore is taking a hard hit. Malaysia and Indonesia are somewhat buffered. Southeast Asia’s importers are now in a 3-4% growth zone. Philippines is already in emergency.

What the region must cope with now is a persistent supply shock with partial financial relief. Although markets can bounce, the real economy won’t rebound in parallel. Global growth prospects are shifting lower to 2.0-2.4%.

What happens in Asia won’t stay in Asia – neither Europe nor North America is immune to the impending tsunami.