We noted in Part 1 that when confronted with the failure of 44 days of bombing Iran “back-to-the-stone-age”and, also, thankfully, being reluctant to send American boots into a Gallipoli-scale slaughter on the ground, the Donald turned to his goofy Secy of Treasury for a 4-D chess move.

To wit, a blockade of the Gulf of Oman, which commenced on April 13th. The latter was supposed to dry-up Iran’s cash flow from global oil sales and to then fill its oil storage tanks full to the rim, thereby causing the pipelines connecting to its 3.5 million b/d oil production apparatus to back up and then explode in a post-constipationary release.

Alas, the Donald’s genius boy band – also including Pete Hegseth and Little Marco Rubio – forget the elephant in the room. To wit, it was always a question of which of the dueling blockades – Iran’s at the Strait of Hormuz or the US Navy’s outside of the SOH on the Gulf of Oman – would run out of time first.

However, you only had to know a little bit about the world’s 103 million barrel per day petroleum supply, demand and storage system, and a tad more about oilfield engineering, production management and storage systems, to realize that there was never a doubt as to the outcome.

Namely, that the true-believers who run Iran, and in the face of an existential threat to their regime, were destined to outlast the world economy’s ability to function without the Persian Gulf’s massive flows of hydrocarbons and its derivatives. These crucial ingredients of global economic life ordinarily transit the Strait of Hormuz (SOH) to the tune of 30 million BOEs (barrels of oil equivalent) each and every day.

Of course, the truth is that the Donald is lazy, impatient and impulsive—and therefore is always ready to run with a factoid or cockamamie notion that suits his purposes at the moment. And regardless of whether it happens to be true, valid, plausible and or even rational.

So when the know-it-all but actually clueless Wall Streeter at the Treasury Department tried to horn-in on the Big Boys action in the White House Situation Room by stumping up his “Operation Economic Fury”, the Donald was all ears. He then assuredly announced that Bessent’s brilliant idea would soon be giving the term “silver bullet” a wholly new definition – even as he patted himself on the back for making it possible:

“The blockade is genius. The blockade has been 100% foolproof. It shows how good our Navy is, I can tell you that. Nobody is going to play games. We have the greatest military in the world, and I built much of it during my first term.”

Except. Except. The prowess of the US Navy wasn’t hardly the half of it. In truth, the blockade was really about oil patch engineering. That and the proven resourcefulness of the Iranian regime when it comes to thwarting attacks on its economy after decades of sanctions, embargoes and malicious economic pressures of every kind.

The Donald was apprised of none of this, of course, so naturally he went ball-to-the-walls, exuberantly promoting the efficacy of the blockade.

“When you have lines of vast amounts of oil pouring through your system, if for any reason that line is closed because you can’t continue to put it into containers or ships… what happens is that line explodes from within, both mechanically and in the earth… They say they only have about three days left before that happens. And when it explodes, you can never rebuild it the way it is.”

Well, three days have passed since the Donald issued the above statement, and nothing has exploded in the Iranian oilfields. And that’s par for the course when it comes to the Donald’s penchant for making up shit and then announcing it to the world.

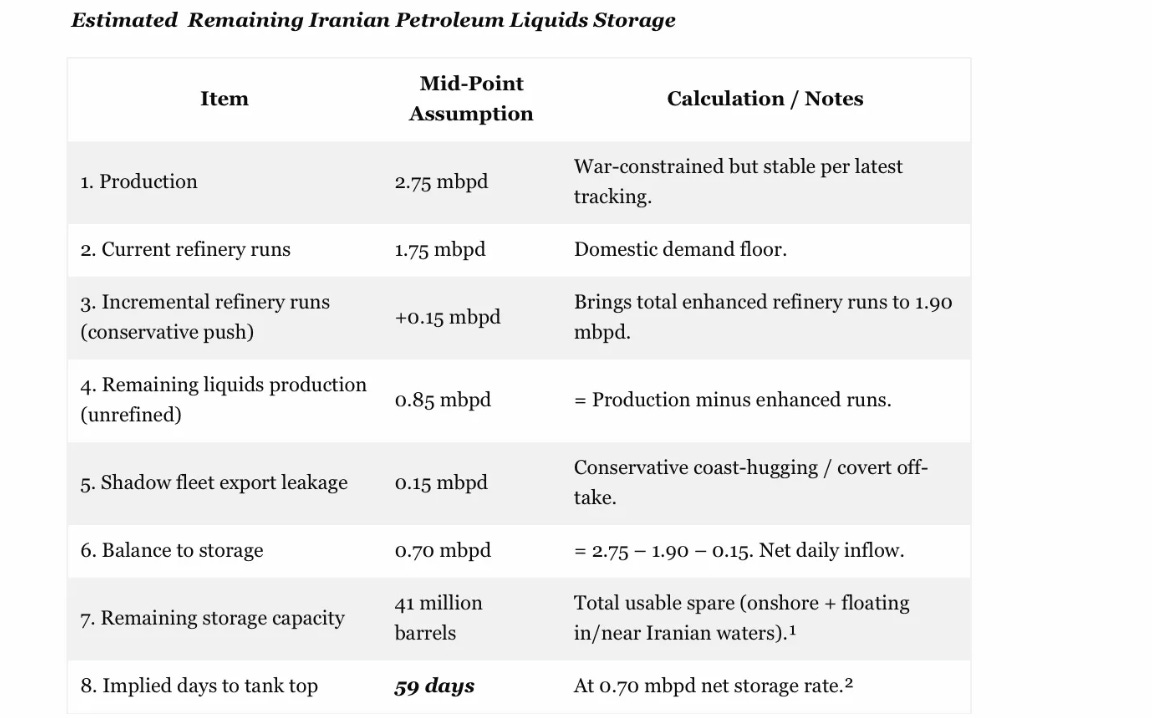

In the first place, there was not a remote chance that Iran’s 41 million barrels of above ground storage tanks would fill to the rim, and then blow up its oil fields in less than three days. As we demonstrated in Part 1, they would have had upwards of 60 days of combined above ground and floating storage – even if production were to remain at the current 2.75 million barrels per day.

But for crying out loud. It doesn’t have to remain there. Iran’s extensive oilfields do not function as some inflexible deus ex machina. Over any reasonable period of time, production levels can be managed significantly higher or lower.

As it happens, however, people who know how to produce 3-5 million barrels per day, as they have over the last decade from Iran’s aging oilfields, would sure as hell know how to carefully reduce production to the level of domestic use (1.75 million barrels/day) plus available storage.

To be sure, throttling back the daily oil lifting rates might well hurt economically via short-run revenue losses and potential future output declines requiring costly restarts. But modulating production levels is a manageable engineering task – not the Donald’s doomsday “lines exploding from within” scenario.

Indeed, oil companies the world over do this during periodic field maintenance, price crashes, or force majeure all the time. The current US blockade, therefore, might create some pain through sustained pressure on exports and storage but not an unmanageable, instantaneous blow-up.

So the blockade was never destined to generate a sudden catastrophic “gotcha” event, as portrayed by Bessent, who knows little about the oil fields and the Donald, who comprehends even less.

Oil production (especially in Iran’s mature fields) can and routinely is managed with gradual rate reductions, flow choking, and planned shut-ins to minimize reservoir and infrastructure damage. The “explosion in three days” scenario is therefore not merely hyperbolic; it’s just plain barking nonsense.

In fact, gradual cutbacks to close the gap between daily output and daily off-take – even with no exports and extremely limited storage – would be readily feasible and well within the range of standard oilfield practice.

So start with the current gap between production at 2.75 mb/d and domestic refinery runs and internal use at about 1.75 mb/d. Even if the enhanced refinery runs and small leakage shown in the table below did not happen, the maximum required cutback from current production levels would be about 35% or 1.0 mb/d. Tops.

{kind=link}

Needless to say, Iran’s petroleum engineers and oilfield managers – especially given several weeks to implement adjustments – have designed their wells, pipelines, and reservoirs with controls for this exact situation. Thus, its wells have adjustable chokes (valves) at the wellhead. Operators can slowly reduce flow rates over hours or days instead of slamming everything shut. This prevents sudden pressure spikes while allowing the reservoir to equilibrate.

Iran could also prioritize this production curtailment process on a field-by-field basis, starting with less critical wells. So if exports stop completely, upstream production doesn’t have to keep pumping at full volume into full tanks/pipelines.

They can throttle back lifting rates to match available storage or domestic use. Many Iranian fields already use gas lift or water/gas injection for pressure support; these systems can be scaled down gradually to avoid disrupting reservoir dynamics.

In fact, they’ve handled temporary large shut-ins before without “explosions.” Standard protocols involve monitoring bottom-hole pressure, injecting inhibitors (to prevent corrosion/scaling), and avoiding abrupt stops that could cause paraffin/wax buildup or sand settling.

Long-term issues (e.g., clay swelling in carbonates, water intrusion, or minor mechanical deformation) are real in mature fields like Iran’s. But they’re mitigable with planning – not irreversible “explosions.”

Similarly, high water-cut wells might need nitrogen lifts or pumps to restart, but that’s routine work-over work, not evidence of a field-destroying crisis. So what the “explosion” claim actually refers to is the risk of pressure buildup in pipelines and reservoirs when off-take flow is blocked downstream while upstream production continues unchecked. In theory, this could lead to over-pressure, clogs, or leaks—but real world systems have safety relief valves, pressure sensors, and automatic shutdowns.

Indeed, oilfield experts note that literal pipeline/well explosions from this kind of hypothetical situation are “nearly impossible”. The real risk is longer-term in the form of forced shut-ins in mature carbonate reservoirs (common in Iran). This could disrupt pressure support from gas re-injection, leading to some permanent productivity loss (e.g., 100k-500k bpd in worst-case selective fields).

But even this kind of potential impairment builds over weeks and months with poor – not standard – management. Moreover, Iran’s fields are not uniquely fragile like ultra-heavy oil (Venezuela) or shale. They’ve restarted after past shut-ins with limited lasting damage.

For example, after the global collapse of oil demand in the spring of 2020 owning to worldwide pandemic lockdowns, Iranian production was reduced by nearly 50% in a matter of months, from 3.75 mb/d to 1.9 mb/d.

Yet after the global economy re-opened and returned to normal petroleum demand levels, production was subsequently restored to pre-war levels at just under 3.5 mb/d during 2024 and 2025.

In short, there is going to be no explosion in the Iranian oil fields. The Donald is chasing yet another delusion ponied up by his utterly incompetent staff.

Between creative expansion of its storage including floating vessels and salt caverns, enhanced refinery runs to bolster the domestic economy, even minor export leakages via its coast-hugging dark fleet and standard oilfield production management, the Iranians are likely to keep their petroleum economy stable and functioning.

So the blockade won’t be a SILVER BULLET to rescue the Donald from his Iranian War folly, either.

Meanwhile, the Donald is yet again waiting for Godot. But he doesn’t have much time left because the other side of the dueling blockade equation is deteriorating fast. That is, not only is oil heading once again to $125 per barrel and $5 per gallon for gas, but the rest of the vast array of industrial commodities which normally flow through the SOH are beginning to take a larger and larger bite out of global economic stability with each passing week.

So the Donald, as usual, is utterly delusional when he plays school yard negotiator, barking at the swing-sets and slides with the refrain “I’ve got all the time in the world.”

He doesn’t. Not even remotely.

In fact, the near-total closure of the Strait of Hormuz since early March 2026 has also created one of the most acute non-oil supply shocks in modern agricultural history, to take the most obvious example.

Roughly one-third of global seaborne fertilizer trade – about 16 million tonnes in 2024 and 2025 – normally transits the SOH from Persian Gulf producers. Accordingly, the Gulf states plus Iran account for 34-49% of globally traded urea, 23-30% of ammonia, 41-50% of sulfur, and 20-26% of phosphate fertilizers (DAP/MAP).

These volumes cannot be easily rerouted: pipelines serve only crude oil, not bulk fertilizers or sulfur, and alternative ports lack capacity or infrastructure. Production has also been directly curtailed by attacks on gas processing infrastructure and feed-stock shortages.

On the nitrogen fertilizer side (urea and ammonium nitrate chains), Qatar’s QAFCO is the world’s largest single-site urea exporter with capacity of 5.4 million tonnes/year or about 10-14% of global exports. But it halted output almost entirely after the LNG/gas plant strikes. Saudi Arabia’s SABIC and other Gulf producers have also seen exports drop sharply.

On a pre-crisis basis the region shipped about 10.5 million tonnes of urea annually (21% of global trade) and supplied India 40% of its urea imports – along with major quantities to Brazil, the USA, Australia, and West Africa. Monthly Arab Gulf urea loadings exceeded 1.5 million tonnes; Iran added another 350,000-400,000 tonnes.

With shipments stalled, urea prices jumped 50%+ within weeks after February 28th (e.g., from $480/tonne to $720/tonne), and ammonia followed. Ammonium nitrate, derived from the same ammonia stream, faces parallel tightness. These nitrogen fertilizers are critical for cereal, oil-seed, and rice crops. The shortages now swelling by the day will force farmers to cut application rates or switch crops, directly lowering yields.

The negative impacts of the SOH closure on the sulfur-phosphate chain is further compounding the ag crisis. Gulf producers (Saudi Aramco, ADNOC, Qatar) supply 41-50% of globally traded sulfur, a byproduct of oil/gas desulfurization and essential feedstock for sulfuric acid.

Sulfuric acid, in turn, converts phosphate rock into water-soluble DAP and MA – which are the world’s go-to yield enhancing fertilizers. In this context, Saudi’s Ma’aden complex is the region’s largest phosphate exporter, accounting for 26% of global DAP trade. Disruptions here ripple far beyond the Gulf to China, Morocco and Indonesia (the major phosphate producers), which rely on Gulf sulfur. So their output is now constrained, as well.

Phosphate prices and NPK blends have surged, hitting West Africa and Latin America especially hard. Overall, analysts estimate 25-38% of global nitrogen/phosphate trade and 45% of sulfur trade are at risk.

The timing is truly catastrophic for “next fall.” Northern Hemisphere spring/summer 2026 planting (already underway in parts of the US, Europe, and Asia) faces immediate shortages, but the bigger shock will likely hit the 2026-2027 crop year fall planting in the Southern Hemisphere (Brazil, Australia, Argentina) and winter wheat cycles in the Northern Hemisphere.

IFPRI and other forecasters warn of 5-15% potential declines in global grain/oilseed yields if fertilizer use drops 10-20% in import-dependent regions.

India (heavily reliant on Gulf urea) and Brazil (key soy/corn exporter) are most exposed. Reduced applications in these two giant ag producers could shrink global harvests by millions of tonnes, tightening global food supplies into late 2026 and 2027.

Food-price inflation is already materializing: urea-driven cost increases are already feeding into higher bread, rice, meat, and vegetable prices. Developing nations therefore face acute food-security risks, including higher import bills, subsidy strains, and possible rationing or unrest.

Even the US and EU, though less dependent, are faced with elevated farm-input costs and secondary effects via global commodity markets. No quick fixes exist. Alternative suppliers (Russia, Egypt, China) cannot scale fast enough, and many face their own export curbs or logistics issues.

In addition, strategic fertilizer reserves are minimal compared to oil stocks. The result is a classic “food security time bomb”. Higher fertilizer prices squeeze margins, reduce planted acres or yields, and cascade into grocery bills and political instability – all likely hitting by fall 2026.

In the case of helium and semiconductors, Qatar supplies 30-36% of global helium as a byproduct of its massive North Field LNG/gas processing. Production at Ras Laffan – the world’s largest helium hub – halted in early March after infrastructure missile strikes and LNG curtailments, removing roughly one-third of world supply overnight.

Helium ships in specialized cryogenic containers that last only 35-48 days before boil-off. Consequently, thousands of containers are now stranded or evaporating. South Korea and Taiwan (largest importers) will face acute shortages first.

Helium is irreplaceable in semiconductor fabrication for wafer etching, plasma processes, and ultra-low-temperature cooling. Chipmakers already report 14-20% export cuts translating into fab-line risks; prices have soared 50%+.

Needless to say, the Chip Shock threatens AI hardware, memory, and advanced logic production at a time of surging demand.

Healthcare (MRI magnets) and aerospace are also being hit. But semiconductors feel the earliest pinch – with potential major output losses in Asia within weeks if stocks run dry.

The Persian Gulf is also a 35-40% player in global petrochemical exports ($20–25 billion annually through SOH). Saudi, UAE, and Qatar export massive volumes of methanol (14 million tonnes/year regionally), monoethylene glycol (MEG, 6.5 million tonnes), polyethylene (PE, 12.5+ million tonnes), polypropylene (PP), and other olefins derived from ethane, propane, and naphtha.

Iran’s 80-90 million tonne petrochemical capacity has also curtailed exports to prioritize domestic needs. Naphtha and LPG feedstock flows to Asia (Japan imports 70%, South Korea 50%) are already being throttled, forcing steam cracker shutdowns in Northeast Asia.

Downstream impacts, of course, cascade into plastics, textiles (MEG for polyester), packaging, automotive parts, and construction resins. Prices for PE, PP, and MEG have jumped by upwards of 10% to 15% in days. Consequently, Asian buyers are scrambling to access US or European alternatives, tightening global polymer markets.

The shocks, in turn, are already reshaping supply chains and inflating costs for everyday goods from bottles to fibers. And given the complexity and length of global supply chains, these effects are expected to persist for months even if shipping partially resumes.

Aluminum and broader industrial sectors are also being impacted heavily. The Gulf smelters (UAE’s EGA at about 2.7 million tonnes, Saudi Ma’aden at about 0.8 million tonnes, Bahrain’s Alba) produce about 9-10% of global primary aluminum, almost all exported via the SOH.

Strikes damaged EGA’s Al Taweelah complex and Alba facilities. So exports have largely halted, with limited truck rerouting to Oman ports proving costly and slow. Raw-material imports (alumina/bauxite) are also being blocked, risking further Gulf smelter production curtailments.

The region supplies about 20% of non-China aluminum to the US, EU, and Asia. Accordingly, LME inventories have already plummeted, while aluminum prices have hit 4-year highs. Overall, the global industry has seen premiums surge and the market flip from pre-war surplus to a growing supply deficit.

Downstream effects from the growing shortage of primary aluminum are rippling into autos, construction, packaging, renewables (solar frames, wind components), and aerospace. Other industrials (e.g., sulfur for metals processing) face collateral pressure.

Combined, these shocks are materially raising manufacturing costs globally, delaying projects, and feeding inflation in finished goods – compounding the fertilizer and petrochemical hits.

Needless to say, recovery in all of these Persian Gulf-fed sectors hinges on Hormuz reopening. In turn, that means the Donald does not have all the time in the world – if any time at all – before widespread “stagflation” spreads globally and laps up on the economic shores of the USA, as well.

David Stockman was a two-term Congressman from Michigan. He was also the Director of the Office of Management and Budget under President Ronald Reagan. After leaving the White House, Stockman had a 20-year career on Wall Street. He’s the author of three books, The Triumph of Politics: Why the Reagan Revolution Failed, The Great Deformation: The Corruption of Capitalism in America, TRUMPED! A Nation on the Brink of Ruin… And How to Bring It Back, and the recently released Great Money Bubble: Protect Yourself From The Coming Inflation Storm. He also is founder of David Stockman’s Contra Corner and David Stockman’s Bubble Finance Trader.No. They aren’t. He made it up. Every damn bit of it.