Pudding River in flood, near Mt. Angel, Oregon. Photo: Jeffrey St. Clair.

With the Federal Emergency Management Agency (FEMA) Review Council’s final recommendations finally available, one particular recommendation stands out. In the section titled, “Shift to Private Market through Depopulation of Existing National Flood Insurance Program (NFIP) Policies,” the council recommends establishing a voluntary “take-out” program that would transfer eligible policies to private insurers — similar to what states like Florida and Louisiana call depopulation programs. There is also a recommendation for a flood insurance marketplace, similar to the Affordable Care Act health insurance marketplace, that would allow private insurers an opportunity to offer coverage to consumers before they consider the NFIP.

There are many issues with these recommendations, especially for high-risk states like Florida, where private insurance is more expensive than NFIP policies and risk-averse companies have been pulling out of the state. But one glaring issue with the report is that the council makes no mention of the Community Rating System (CRS) and how a voluntary “take-out” program would affect it.

What is the CRS?

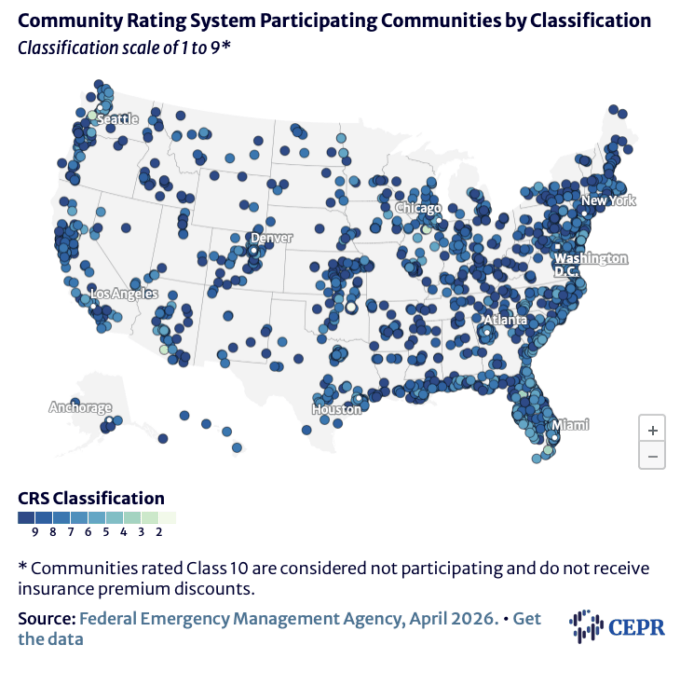

To be covered by an NFIP flood insurance policy, a property must be located in a community participating in the NFIP. Currently, over 22,300 communities across the US participate. CRS, however, is a voluntary incentive program established in 1990 that allows residents in those communities to receive discounted premiums if the community invests in flood mitigation that exceeds NFIP’s minimum requirements. Currently, a little over 1,700 communities across the US have a CRS classification (Figure 1).

Figure 1

CRS discounts reflect the amount of work the community has done in three areas: promoting extensive floodplain management; bolstering the NFIP through mapping and information collection that identify risk and enable accurate actuarial rating; and minimizing or preventing harm to insured property.

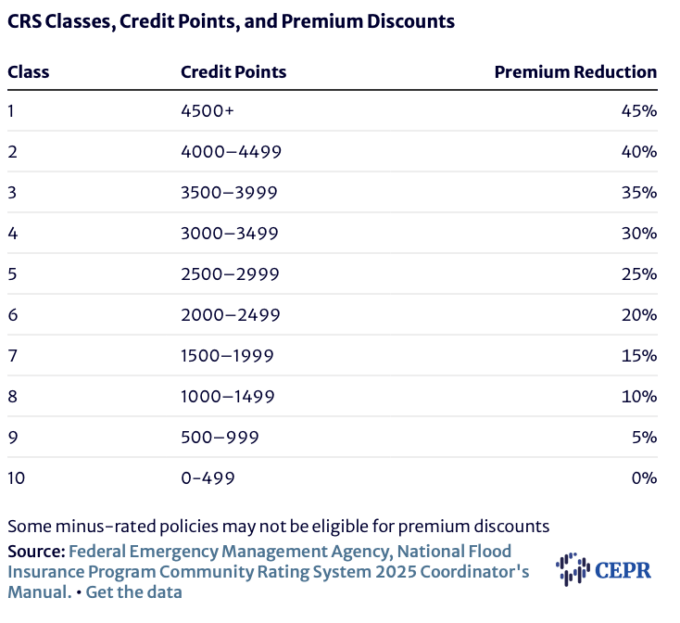

Participating communities receive credit points based on their 19 creditable activities across the categories of public information, mapping and regulations, damage reduction activities, and warning and response. Based on the number of activities completed, communities receive a class rating from 1 to 10, with Class 1 communities receiving the largest discount and Class 10 communities receiving no discount (Table 1).

Table 1

Research has found that CRS not only reduces flood losses overall but, in some high-risk Gulf Coast states, participation in the program reduces flood damage by almost 6 percent in Class 5 communities. Experts have found that despite the high costs to NFIP from severe flood events such as hurricanes, “CRS will become crucial in mitigating damages and will yield greater net benefits to the NFIP.”

So, What is the Problem?

A major component of the CRS is encouraging more NFIP communities to participate, thereby reducing the program’s overall risk. One of the creditable activities is “Assessing flood insurance coverage in the community and implementing a plan to promote flood insurance.” One could interpret this as any kind of flood insurance, private or NFIP. However, private insurers generally ignorecommunity-wide CRS ratings, opting instead to employ their own proprietary risk modeling to price properties on an individual basis. If you live in a low-risk area, that’s great news. In a high-risk area, not so much.

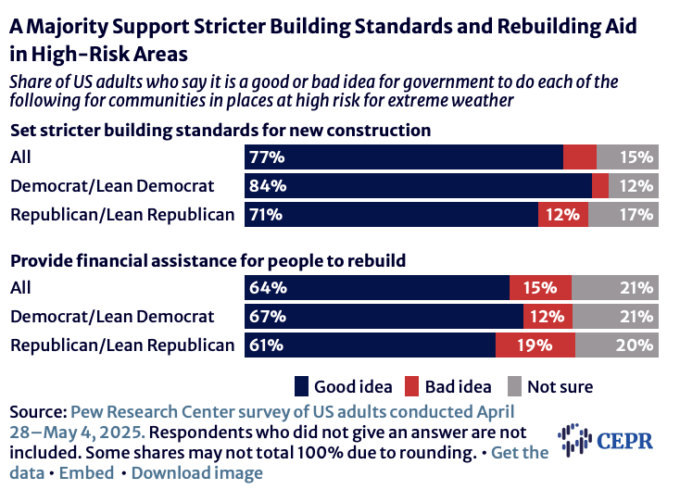

As we featured in our Majority Agenda series of policy briefs, polling shows that Americans want the government to do more to build resilience, not encourage less through privatization. In fact, 64 percent of Americans think the government should provide financial assistance for people in high-risk areas to rebuild after a disaster, which can take the form of FEMA public and individual assistance as well as insurance (Figure 2). If the government wants to lower those costs, that means incentivizing not just homeowners but also communities to undertake mitigation measures.

Figure 2

The vagueness of the FEMA Review Council’s recommendations is concerning. There is a definite throughline in their report that the council and the administration believe states should do more and the federal government should do less. But by putting programs like the NFIP at risk, the path to disaster recovery becomes increasingly fraught for Americans — particularly as broader economic pressures, including rising prices and persistent inflation, continue to squeeze consumers. Increasing insurance costs mean people will forgo coverage entirely, and the purpose of FEMA’s post-disaster individual assistance program is to assist the uninsured and underinsured survivors. In essence, more people will seek government relief for a problem the government has essentially decided it’s not obligated to solve.

Programs that promote mitigation, like the CRS, should be protected, whether that’s through state-level legislation that links private flood insurance to the CRS or by ensuring the NFIP remains adequately funded at the federal level instead of moving toward privatization. After all, if the federal government can spend $30 billion and counting on one war, it can spare some money to help Americans.

This first ran on CEPR.