With the U.S.-led Pax Silica framework, the Philippines is becoming a dual-use platform where military strategy and supply-chain restructuring are converging.

Over the past year, the Philippines has moved decisively into the front line of US–China friction, thanks to expanded access under the bilateral Enhanced Defense Cooperation Agreement (EDCA), large-scale military exercises near Taiwan-adjacent waters, and growing interoperability with U.S. forces.

The Philippines is transitioning toward a logistics hub in a possible regional contingency. What is new is that this military alignment is now paired with an economic architecture: Pax Silica.

Pax Silica, a risk multiplier

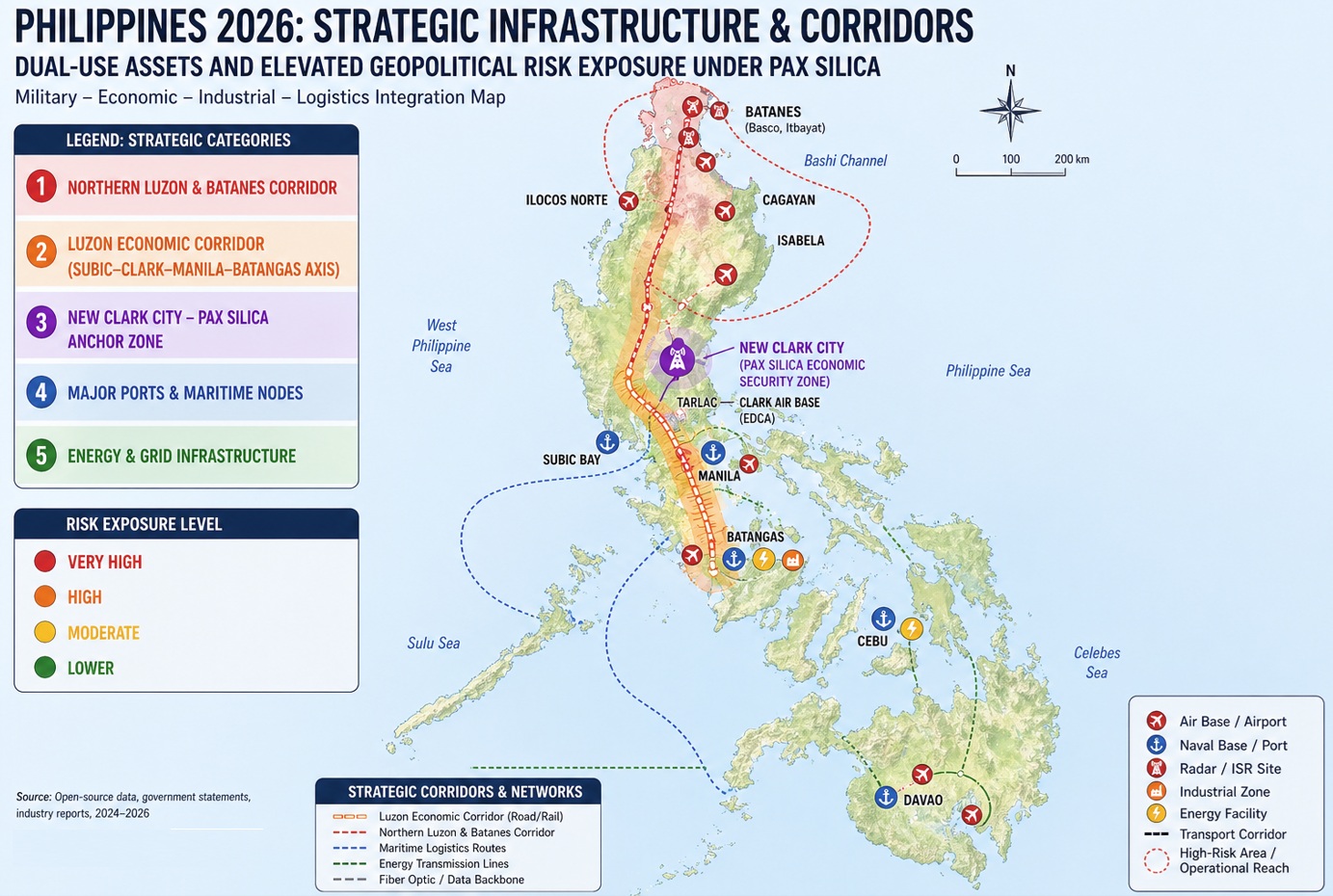

In April 2026, the Philippines joined the U.S.-led coalition designed to secure supply chains in semiconductors, AI infrastructure, and critical minerals. The centerpiece is the planned 4,000-acre “Economic Security Zone” in the Luzon Economic Corridor, intended as a hub for allied manufacturing and resource processing.

In the Philippines, Pax Silica is sold as an opportunity; a chance to climb the value chain, attract investment, and leverage mineral endowments. The country’s large nickel and cobalt reserves, its workforce, and its strategic location make it an attractive node in this emerging network. That’s the pitch.

In isolation, this could be a development breakthrough. But Pax Silica does not operate in isolation. It is explicitly designed to decouple supply chains from China and consolidate them within a U.S.-aligned bloc.

That means participation in a geoeconomic divide that could reshape trade flows, investment patterns, and political risk for decades.

Investment and trade risks

The economic implications follow through several channels. First, investment. The Philippines will likely see targeted inflows tied to Pax Silica – particularly in minerals processing, electronics, and logistics.

But these inflows will be conditional and politically anchored. Meanwhile, broader investment will face rising risk premiums as the country is reclassified from a conventional emerging market to a geopolitical frontline state.

Investors will not ignore the fact that key infrastructure now serves both commercial and strategic purposes.

Second, trade. The Philippines’ economic structure is deeply entangled with China, which absorbs the majority of its raw nickel exports and remains a major trading partner.

Pax Silica’s goal of rerouting supply chains away from China is likely to amplify trade diversion and friction.

Corruption and militarization of infrastructure

Third, energy and supply vulnerability. In a gray-zone escalation, even limited economic leverage by an adversary could trigger inflation shocks in the import-dependent economy.

In the short term, Pax Silica increases exposure to retaliatory pressure.

In the Philippines, the Iran crisis has caused a severe crisis and national energy emergency. But it pales in comparison to the possible long-term implications of Pax Silica.

Fourth, and most critically, the Philippines enters this transition with weak state capacity, as evidenced by large-scale corruption in infrastructure projects.

This matters because Pax Silica and military alignment both depend on the same foundations: ports, logistics corridors, energy systems, and procurement processes. Since these are known to be compromised by corruption and inefficiency, the risks are magnified.

Bases, ports, and industrial zones linked to Pax Silica are no longer just economic assets. They are now potential strategic targets in an escalation scenario.

Economic backbone as a dual-use target

In light of Pax Silica, the Philippine map of expanding military targets no longer consists only of traditional bases like EDCA sites. It now includes:

- Northern Luzon and Batanes corridor: proximity to Taiwan, staging ground for logistics and surveillance

- Subic–Clark–Manila–Batangas axis (Luzon Economic Corridor): now the core of Pax Silica industrial development and transport infrastructure

- New Clark City: likely site of the 4,000-acre economic security zone, combining industrial and logistical functions

- Major ports and energy nodes integrated into allied supply chains

These are dual-use targets: both economic assets and strategic infrastructure.

Pax Silica effectively expands the definition of what counts as a “target” from purely military installations to the broader economic backbone of the country.

So, where do we go from here?

{kind=link}

Ominous scenarios

In the Managed Alignment scenario, the country deepens its role in both military and supply-chain networks without triggering major conflict. Growth continues at a moderate pace – roughly 4.5 to 5.5% – but below potential. Pax Silica delivers selective gains, but these are offset by higher risk premiums and trade frictions.

In the Gray-Zone Escalation scenario, tensions intensify without open war. Economic coercion, supply disruptions, and political pressure become routine. Growth slows to 3–4% percent, investment stagnates, and volatility increases.

This is the path to long-term underperformance. Its main beneficiaries are military and security elites and oligarchic dynasties that own the strategic infrastructure.

The Marcos Jr government likely sees itself in a mild Managed Alignment scenario. In terms of economic realities, it may be somewhere between that scenario and the Gray-Zone Escalation scenario.

There is also a third possible scenario, Strategic Rebalancing. It seeks to reduce exposure while emphasizing ASEAN neutrality. It would offer the best economic outcomes to the Filipino people.

Launched by former president Duterte, it is currently a low-probability scenario. An election triumph by Vice President Sara Duterte would make it topical again.

Brave new Philippines?

The most immediate challenge is a status quo in which the Gray-Zone Escalation would morph into a Taiwan conflict spillover. Unfortunately, the Philippines’ new dual role – as a military hub and a Pax Silica supply-chain node – amplifies its exposure.

Economic contraction, capital flight, and infrastructure disruption would follow, as the very assets intended to drive growth become liabilities.

The Philippines is entering a new phase of moderate growth under persistent geopolitical drag, where gains from integration into allied supply chains are offset by higher risk, reduced flexibility, and ongoing governance challenges.

The real cost of the current path would be a transformation into a frontline node in potential Taiwan conflict, where every Philippine port, factory, and corridor carries both economic promise and strategic risk.

The original commentary was published by The Manila Times on April 27, 2026.